By Ryan Yuhnke

Wouldn’t it be nice if you could predict the movements of the market exactly and only experience gains instead of losses? Unfortunately, this is a scenario that will never happen. What can happen, however, is having a loss-mitigation strategy in place if and when the indicators of market turmoil start to rear their heads.

Did you have a sell strategy in place during the brutal bond market performance of 2022? Do you have one now? There are many intermediate and long-term bond investors out there shaking their heads and wondering what to do with the steep losses they experienced and if they’ll see a rebound. Read on to learn more about why a sell strategy in bonds is crucial and how you can prepare for future volatility.

Hindsight Is 20/20

When to Buy

With perfect 20/20 hindsight, the best time to own bonds is when interest rates are high and falling. This is because bond prices are inversely related to interest rates. If you own an existing bond with a high interest rate during a time when interest rates are falling, your bond will become more valuable.

Think of it this way: When you borrow money to buy a house, you want to lock in the lowest 30-year fixed rate possible. So maybe that was near or below 3% in the past few years. When you own bonds, on the other hand, you are lending money instead of borrowing. You can lend the funds to the U.S. government, companies, municipalities, etc. Since a bond investor is locking in a fixed rate for funds they are receiving, they want the rate to be as high as possible.

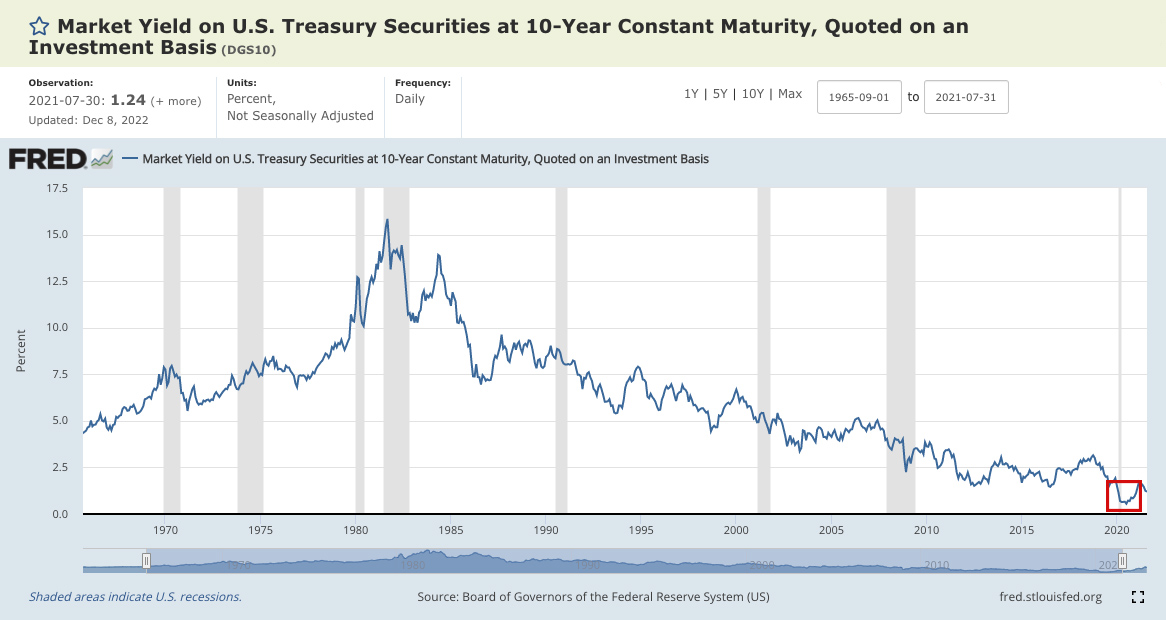

Looking back, September 1981 would have been an ideal time to buy a long-term U.S. government bond. If you bought at that time, you would have locked in a 15.84% annualized return for 10 years, as you can see on the chart below.

When to Sell

Again with perfect 20/20 hindsight, the best time to sell bonds is when interest rates have reached a low and are gearing up to rise significantly. If you sell right before rates increase, your bond will be valuable to sell because its fixed rate is higher than the current market rate. Once rates rise, however, the value of your bond will fall and investors will have the opportunity to buy new bonds at higher rates. This move in prices and yields is what occurred in 2022 and has continued into 2023. Not understanding interest rate risk is why SVB bank went out of business and was just taken over by the government. They purchased and owned longer term US government bonds yielding a low rate of nearly 1.8% and when they needed funds were forced to sell these bonds at a loss of $1.8 billion dollars.

Looking at the chart again, we see that the best time to sell intermediate-term bonds (those with a maturity of around 10 years) was in July 2020, when the 10-year U.S. Treasury bond was .55%. If you had purchased that bond in July of 2020 with $10,000, you would have received $55 per year in interest for 10 years, and 10 years later you would receive your $10,000 back. Sounds like a TERRIBLE deal especially when taxes are considered. Instead of just sitting in bonds and waiting to experience the credit or liquidity risk and possible loss of value, an informed and sophisticated investor would have sold bonds when rates were near zero and credit spreads were tight and waited in cash for the interest rates to rise.

The bottom line is that the Fed clearly announced that they were not going to allow interest rates to go negative or drop below zero. So, in hindsight, selling longer-maturity bonds when rates dropped well below 1% was the best and only smart option. Many investors held out hope that their bonds would retain value, or just didn’t understand how rising rates could impact their portfolios. But holding on to bonds when interest rates were near zero, is like trying to get that extra 2% of juice from the orange when you have already received 98% of it. Not having a sell strategy and looking for every last drop may have cost you significant losses in 2022 and 2023.

What to Do Now

From an interest rate perspective, investors who own intermediate or longer-term bonds want and need longer-term interest rates to go down. If you own a bond fund and follow the “hope and pray” strategy, or you chase past performance, you could be setting yourself up for further losses. The value of your bonds will not come back if rates keep going up, up, up.

If we fall deeper into a recession and those longer rates do go down, then you will see a gain. So the biggest question for bond investors is “Which direction will rates move for the length of bonds you own?” Looking back, if you didn’t sell somewhere when rates were near 1% or below, then you didn’t have a sell strategy. Do you have one now?

Partner With a Professional

At Court Investment Services, we helped bond investors with a proactive sell strategy and weren’t caught flat-footed when interest rates rose. For the past 2 years, bonds have been most impacted by the sudden steep rise in interest rates, but as we enter a recession in 2023, what will be more important to pay attention to is CREDIT RISK. We will address this in another follow-up article.

If you are managing probate or trust assets with bonds and would like some guidance on your strategy, please reach out to us! Schedule an appointment by contacting us at (800) 880-2760 or Kitty at kchu@CourtInvestmentServices.com. And if you would rather invest with a 5% annualized return and no interest rate or credit risk, read our other article on short-term U.S. debt.

About Ryan

Ryan Yuhnke is founder and Principal at Court Investment Services, an independent, fee-based investment firm that serves attorneys and fiduciaries as they manage estate-held assets. With two decades of experience, Ryan’s proactive, relationship-based process saves his clients time and money while putting them first in everything. He provides services and support to help attorneys and professional partners oversee and manage special-needs trusts, estates, conservatorships, guardianships, and other court accounts, including IRAs, 401(k)s, and all manner of retirement accounts that also fall under his clients’ management. Ryan is known for his commitment to excellence and transparency and his deep knowledge of probate laws, court compliance, and strategies to keep assets safe while abiding by all court and probate code directives. Ryan’s goal is to make his clients’ lives easier, providing investment support and education along the way.

Ryan has a bachelor’s degree in economics from the University of California, Irvine, and built his career working in banks, national investment firms, and registered investment advisory firms (RIAs.) Prior to starting CIS, he earned the title of First Vice President, and Portfolio Management Director while employed at Morgan Stanley in Newport Beach, CA. When he’s not working, Ryan can be found traveling to experience new cultures and environments, focusing on personal development through mental, social, spiritual, emotional, and physical growth, and most importantly enjoying quality time and creating new memories with family and friends. To learn more about Ryan, connect with him on LinkedIn.